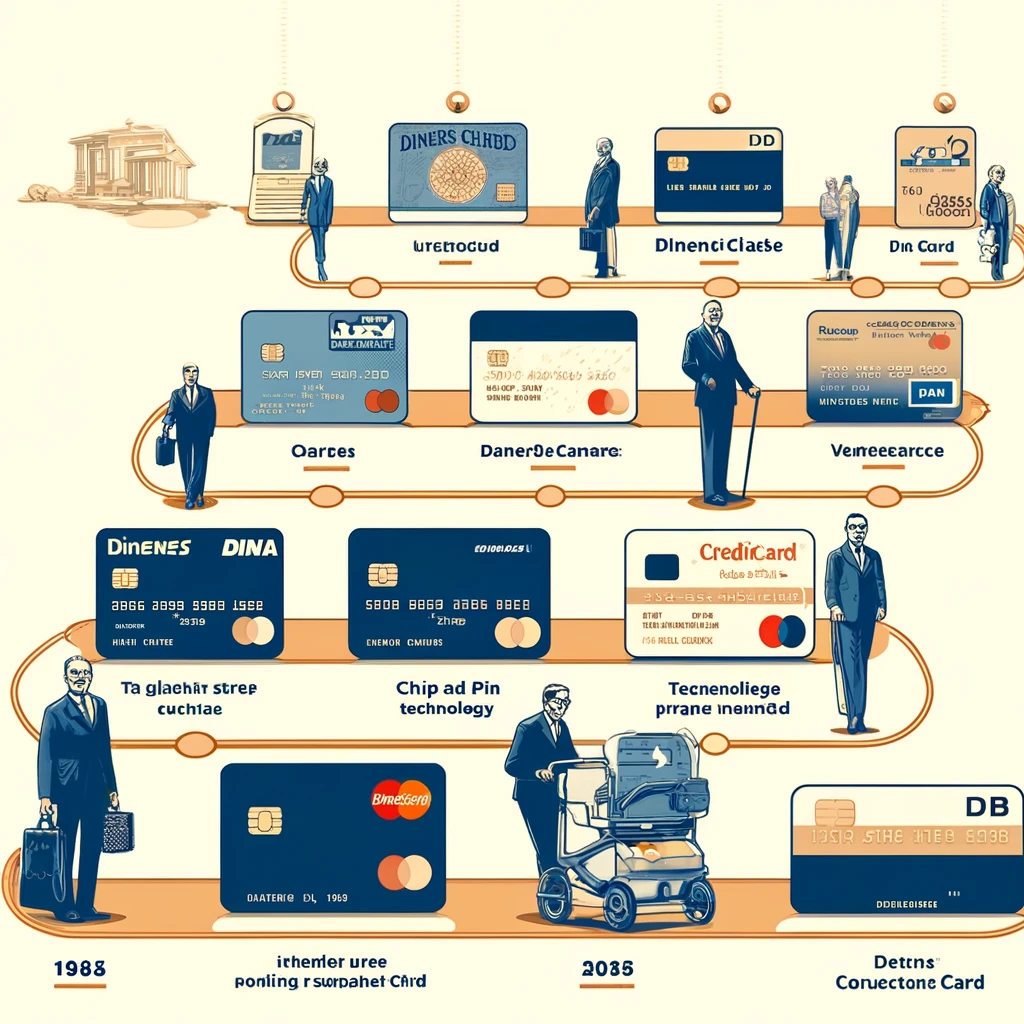

Credit cards are an integral part of our daily lives, offering convenience, security, and a host of financial benefits. However, these small pieces of plastic have a history that spans over a century. From their humble beginnings with the Diners Club card to the sophisticated modern-day credit cards, the evolution of credit cards reflects broader changes in technology, consumer behaviour, and financial services. We explore the history of credit cards, tracing their development from early charge cards to the versatile financial tools we use today.

The Beginnings: Early Charge Cards

Store Credit and Charge Plates

The concept of credit has been around for centuries, with merchants extending credit to trusted customers long before the advent of plastic cards. In the early 20th century, some department stores and oil companies began issuing metal charge plates and paper cards to their regular customers. These early charge cards allowed customers to make purchases on credit and pay off the balance at a later date. Each store had its own card, which could only be used at that particular establishment.

The Charge-a-Plate

The Charge-a-Plate, introduced in the 1920s, was one of the first forms of a credit card. It was a metal card embossed with the customer’s name, address, and account number. The Charge-a-Plate was used primarily by department stores and worked similarly to a modern charge card, where the store would keep a record of the purchases and bill the customer later.

The Birth of the Diners Club Card

The First Multi-Purpose Charge Card

The modern credit card as we know it began with the Diners Club card, introduced in 1950. Frank McNamara, along with his partner Ralph Schneider, created the Diners Club card after McNamara forgot his wallet during a business dinner and was unable to pay the bill. They envisioned a card that could be used at multiple establishments, allowing members to dine out without carrying cash.

How It Worked

The Diners Club card was initially accepted at 27 New York City restaurants and had 200 cardholders. Cardholders would present the card at participating restaurants, and the restaurant would bill Diners Club. Diners Club would then bill the cardholder, who was expected to pay the full balance each month. The Diners Club card was a charge card, not a credit card, as it required payment in full rather than allowing revolving credit.

Rapid Growth

The Diners Club card quickly gained popularity, expanding to other cities and adding more establishments to its network. By the end of the 1950s, Diners Club had over 20,000 cardholders and was accepted at thousands of locations worldwide. This success demonstrated the viability of multi-purpose charge cards and paved the way for future innovations.

The Emergence of Bank-Issued Credit Cards

Bank of America’s BankAmericard

In 1958, Bank of America launched the BankAmericard in Fresno, California. This was the first bank-issued credit card and marked a significant shift in the credit card industry. Unlike charge cards, the BankAmericard allowed cardholders to carry a balance and make monthly payments, thus introducing the concept of revolving credit.

The Interbank Card Association and Master Charge

Following the success of the BankAmericard, other banks sought to enter the credit card market. In 1966, several banks formed the Interbank Card Association (ICA) to create a unified network for credit card transactions. This collaboration led to the creation of the Master Charge card, which later became MasterCard. The ICA facilitated the acceptance of Master Charge cards at a wide range of merchants, making credit cards more accessible to consumers.

The Evolution of BankAmericard to Visa

In 1976, BankAmericard underwent a major rebranding, becoming Visa. The name change reflected the card’s global reach and the network’s expansion beyond the United States. Visa became synonymous with universal acceptance and reliability, cementing its position as a leader in the credit card industry.

Technological Advancements: The Magnetic Stripe and Beyond

Introduction of the Magnetic Stripe

The introduction of the magnetic stripe in the 1970s was a significant technological advancement for credit cards. The magnetic stripe, invented by IBM, allowed for the storage of account information on the card itself. This innovation made transactions faster and more secure, as the data could be read electronically by point-of-sale terminals.

The Chip-and-PIN Technology

In the 1990s, credit card security took another leap forward with the introduction of chip-and-PIN technology. Also known as EMV (Europay, MasterCard, and Visa), this technology embedded a microchip in the credit card that stored encrypted account information. Cardholders had to enter a personal identification number (PIN) to complete transactions, adding an extra layer of security and reducing fraud.

The Digital Revolution: Contactless Payments and Mobile Wallets

Contactless Credit Cards

The early 2000s saw the rise of contactless credit cards, which use near-field communication (NFC) technology to enable quick and convenient payments. Cardholders can simply tap their card on a contactless-enabled terminal to complete a transaction. This innovation has made transactions faster and more convenient, particularly for small purchases.

Mobile Wallets and Digital Payments

The proliferation of smartphones has led to the development of mobile wallets and digital payment solutions. Services like Apple Pay, Google Pay, and Samsung Pay allow users to store their credit card information on their smartphones and make payments using NFC technology. These digital wallets offer enhanced security features, such as biometric authentication, and provide a seamless and convenient payment experience.

Credit Cards in the Modern Era

Rewards and Perks

Modern credit cards offer a wide range of rewards and perks, catering to diverse consumer needs. From cashback and travel rewards to premium benefits like airport lounge access and concierge services, credit cards have evolved into powerful financial tools that provide significant value to cardholders.

Enhanced Security Measures

Credit card security has continued to improve with advancements such as tokenization, which replaces sensitive card information with a unique identifier or token during transactions. This reduces the risk of data breaches and fraud. Additionally, real-time fraud detection systems and enhanced encryption techniques have made credit card transactions more secure than ever.

Regulation and Consumer Protection

In recent years, there has been a growing emphasis on consumer protection and regulation in the credit card industry. Laws such as the Credit Card Accountability, Responsibility, and Disclosure (CARD) Act of 2009 in the United States have introduced measures to protect consumers from unfair practices and ensure transparency in credit card terms and conditions.

The Future of Credit Cards

The credit card industry continues to evolve, driven by technological advancements and changing consumer preferences. Here are some trends that are shaping the future of credit cards:

Integration with Fintech

Fintech companies are playing an increasingly significant role in the credit card industry. Innovations such as artificial intelligence, machine learning, and blockchain technology are being integrated into credit card services to enhance security, streamline processes, and offer personalized experiences.

Biometric Authentication

Biometric authentication methods, such as fingerprint recognition and facial recognition, are becoming more prevalent in credit card security. These technologies provide a higher level of security and convenience, reducing the risk of fraud and making transactions more seamless.

Sustainable and Eco-Friendly Cards

There is a growing trend towards sustainability in the credit card industry. Some issuers are offering eco-friendly credit cards made from recycled materials or incorporating environmentally conscious practices into their operations. Consumers are increasingly seeking cards that align with their values and support sustainable initiatives.

Digital and Virtual Cards

Digital and virtual credit cards are gaining popularity, offering enhanced security and convenience. These cards can be issued instantly and used for online and mobile payments, reducing the reliance on physical cards. Virtual cards also offer features such as single-use numbers and spending controls, providing added security for online transactions.

Conclusion

The history of credit cards is a show of the continuous evolution of financial services, driven by innovation and changing consumer needs. From the early days of the Diners Club card to the sophisticated and secure digital payment solutions of today, credit cards have transformed the way we manage our finances and make transactions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment